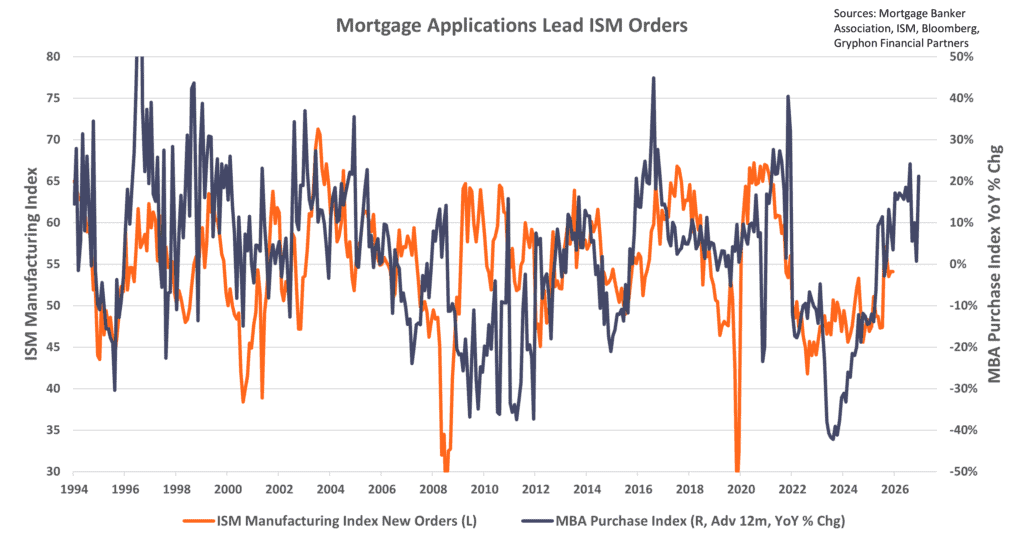

Mortgage applications are often overlooked in favor of more widely followed indicators, but they provide an important early signal about the direction of the US economy. The Mortgage Bankers Association reported that total mortgage application volume has risen roughly 6% year over year in recent weeks, with purchase applications up about 4% and refinance activity increasing more than 10% as mortgage rates have drifted closer to the low 6% range. While application levels remain below the peaks seen during the pandemic housing boom, the recent upward trend suggests that demand for housing is stabilizing and gradually improving. Because mortgage applications reflect buyer intent rather than completed transactions, they tend to move ahead of existing home sales and provide a forward looking view of housing activity.

The connection between mortgage applications and broader economic indicators becomes even more important when considering their relationship with ISM manufacturing new orders. Historically, changes in housing demand ripple into manufacturing through demand for building materials, appliances, furniture, and home improvement goods. Research from the Federal Reserve and Institute for Supply Management shows that housing related activity can lead manufacturing new orders by several months. When more households apply for mortgages, it signals future home purchases and renovations, which in turn generate orders for manufactured goods. Recent ISM data shows new orders returning to expansion territory near the 52 level after spending much of the past two years below 50, indicating improving demand conditions in the manufacturing sector.

The recent increase in mortgage applications therefore aligns with the gradual recovery seen in manufacturing surveys. For example, regional Federal Reserve bank surveys such as the Philadelphia Fed and ISM subcomponents both show rising demand for durable goods tied to housing, including wood products, machinery, and household equipment. As mortgage applications rise, builders and suppliers begin to anticipate stronger demand, which leads to increased production planning and new orders. This dynamic reinforces the idea that housing is not an isolated sector but a leading driver of activity across multiple parts of the economy. Even modest gains in housing demand can translate into meaningful improvements in manufacturing momentum.

From a macroeconomic perspective, the rise in mortgage applications carries balanced but constructive implications. On one hand, higher application activity suggests that consumers are gaining confidence in their financial position, supported by steady job growth and rising incomes. On the other hand, the pace of increase remains measured, which reduces the risk of overheating in housing or a rapid surge in inflation tied to shelter costs. The broader economy benefits from this type of gradual improvement because it supports growth without creating significant imbalances. Additionally, as manufacturing new orders strengthen, businesses may increase hiring and capital spending, further reinforcing economic expansion.

Looking ahead, mortgage applications will remain a key indicator to watch for signals about both housing and industrial activity. If applications continue to trend higher, it would likely support further gains in ISM manufacturing new orders and contribute to a more resilient economic outlook. However, the trajectory will depend on mortgage rates, credit availability, and consumer confidence. Current forecasts from the Mortgage Bankers Association anticipate modest growth in purchase applications through the remainder of 2026, which aligns with expectations for steady but not rapid economic expansion. Taken together, the data suggests that rising mortgage applications are helping to lay the groundwork for broader economic stability rather than signaling either a sharp acceleration or a downturn.

Sources: Mortgage Bankers Association, Institute for Supply Management, Federal Reserve Bank surveys, Federal Reserve Economic Data FRED, National Association of Home Builders, Bureau of Economic Analysis.

Disclosure

This material is provided by Gryphon Financial Partners, LLC (“Gryphon”) for informational purposes only. It is not intended as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy, or investment product. Facts presented have been obtained from sources believed to be reliable, though Gryphon cannot guarantee their accuracy or completeness. Gryphon does not provide tax, accounting, or legal advice. Individuals should seek such guidance from qualified professionals based on their specific circumstances.